There are several well-known tax deferral and mitigation strategies within real estate investing. Most popular is the long-standing Internal Revenue Code (IRC) Section 1031 Exchange that provides a vehicle for deferring capital gain taxes while disposing of investment property.

Other tax savings mechanisms allow real estate investors to potentially eliminate, instead of just defer, some or most capital gain taxes (e.g. IRC Section 170 Bargain Sales). These can be paired with strategic measures, like front loading depreciation through a Cost Segregation Study, to allow the investor to take advantage of future depreciation benefits in advance.

The point here is that you have options. And the best thing to do is work with professionals who understand those options. Our team offers a full-service approach. If you don’t have a real estate or tax professional, we can connect you with one. If you do, that’s great! We’ll work with them too.

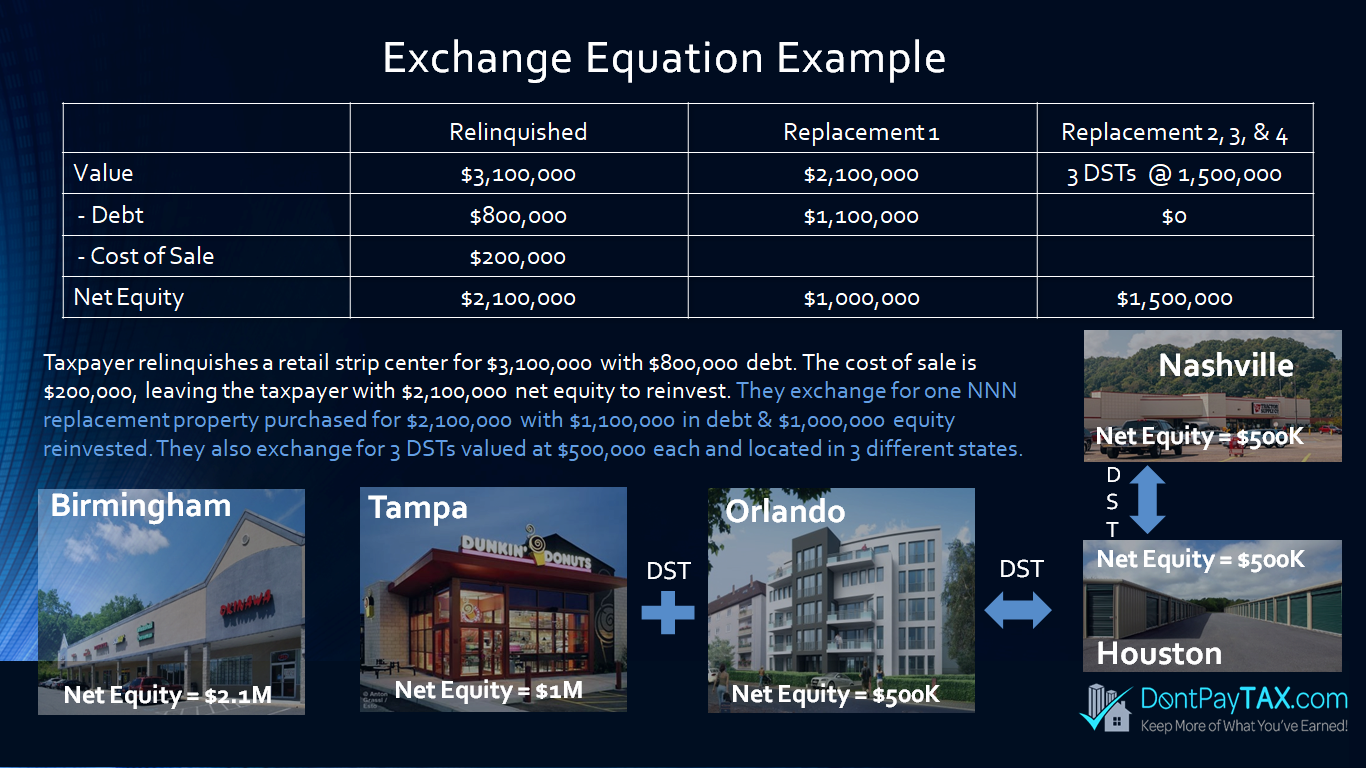

If you’re looking to exit real estate altogether but don’t want to pay the capital gain taxes of a traditional sale (which can be a third or more of your proceeds!), then you can still use a 1031 Exchange and go completely passive on the replacement purchase using a Delaware Statutory Trust (DST). This option is becoming very popular among investors looking to reduce or eliminate active property management burdens while gaining the advantages of partial deed ownership in a diversified and professionally managed portfolio. The DST structure provides ownership of class “A” institutional grade real estate for those who wouldn’t be able to afford it on their own.

First choice, or last resort? DSTs can actually be either. They’re a first choice for those looking to become completely passive real estate owners, potentially receive monthly revenue, and avoid the “3-T” burden of active ownership (Tenants, Turnover, and Trash). DSTs can also serve as last resort ID replacement property to ensure a full tax deferral in a 1031 Exchange because they are more likely to successfully ID and close within the strict timelines required (ID within 45 days, close within 180). This is only for certain investors. If you’re interested in more information, we’ll connect you to a licensed financial securities professional now. Schedule an appointment online.

Other tax savings mechanisms allow real estate investors to potentially eliminate, instead of just defer, some or most capital gain taxes (e.g. IRC Section 170 Bargain Sales). These can be paired with strategic measures, like front loading depreciation through a Cost Segregation Study, to allow the investor to take advantage of future depreciation benefits in advance. Cost Segregation & 1031 Exchanges can be combined to maximize the cash flow of your investments.

The point here is that you have options. And the best thing to do is work with professionals who understand those options. Our team offers a full-service approach. If you don’t have a real estate or tax professional, we can connect you with one. If you do, that’s great! We’ll work with them as a team. If you’re interested in more information, let us connect you to Mr. Biggs #The1031ExchangeGuy, who is a 1031 Training Expert, holding both professional licenses in financial securities and real estate sales.

If you’re looking to exit real estate altogether but don’t want to pay the capital gain taxes of a traditional sale (which can be a third or more of your proceeds), then it is possible for you to use a IRC Section 1031 Tax-deferred Exchange (1031 Exchange) but go completely passive on the replacement purchase side of the exchange. This option can allow for either full or partial tax deferral after the disposition sale of investment real estate, and can give investors a welcomed reprieve from the normally strict deadlines of performing a traditional property to property exchange, beholden to finding quality properties in a very short timeline (45 calendar days from closing on the relinquishing property sale).

The important thing to remember is that performing a 1031 Exchange is a long-term decision! If you ever make a traditional sale on your 1031 replacement property in the future, the deferred capital gains rolled in compounds with the current capital gains due on the sale potentially creating an even larger tax bill than before! That might be acceptable if you intend to play through until death so the heirs can get a step-up in tax basis. But if that’s not the plan, or if the potential of finding an acceptable replacement property isn’t promising, then you should consider either the Delaware Statutory Trust (DST) option (See “Popular Replacements” tab for more specific information on DSTs) or the option below, depending on your specific tax scenario and set of circumstances leading up to this sale.

If you’re looking to exit real estate altogether but don’t want to pay the capital gain taxes of a traditional sale (which can be a third or more of your proceeds), then you can still use a 1031 Exchange and go completely passive on the replacement purchase using a Delaware Statutory Trust (DST) option if you qualify as an accredited investor.

This option is becoming very popular among investors looking to reduce or eliminate active property management burdens while gaining the advantages of potential partial deed ownership in a diversified and professionally managed portfolio. The DST structure provides a creative solution to real estate investors to potentially diversify some of their risk of owning real estate, and for those investors wouldn’t be able to afford class “A” institutional grade on their own. Diversification is accomplished between numerous sectors, asset classes, and geographical locations. Flexibility of utilizing these as a stand alone full tax deferral replacement option, or a partial tax deferral option to limit the tax exposure of an upcoming disposition sale of investment real estate make DST’s an ever increasing popular solution to the strict, unforgiving timelines of a 1031 Exchange.

What is DELAWARE STATUTORY TRUST (DST)?

DSTs can actually be either. They’re a first choice for those looking to become completely passive real estate owners, potentially receive monthly revenue, and avoid the “3-T” burden of active ownership (Tenants, Turnover, and Trash). DSTs can also serve as last resort ID replacement property to ensure a full tax deferral in a 1031 Exchange because they are more likely to successfully ID and close within the strict timelines required (ID within 45 days, close within 180). This is only for certain investors. If you’re interested in more information, we’ll connect you to a licensed financial securities professional now.

“Nearly 35 million Americans live in areas designated as Opportunity Zones. These communities present both the need for investment and significant investment opportunities.”

– US Treasury

Internal Revenue Code (IRC) Section 170

In the United States, a conservation easement (also called conservation covenant, conservation restriction or conservation servitude) is a power invested in a qualified private land conservation organization (often called a “land trust”) or government (municipal, county, state or federal) to constrain, as to a specified land area, the exercise of rights otherwise held by a landowner so as to achieve certain conservation purposes. It is an interest in real property established by agreement between a landowner and land trust or unit of government. The conservation easement “runs with the land”, meaning it is applicable to both present and future owners of the land. As with other real property interests, the grant of conservation easement is recorded in the local land records; the grant becomes a part of the chain of title for the property.

Internal Revenue Code (IRC) Section 170